Ding Yifan, Senior Fellow of Taihe Institute

Shi Junqi, Research Assistant of Taihe Institute

Introduction:

During US President Joe Biden’s trip to Europe, the United States and the European Commission reached an agreement to conduct strategic energy cooperation, aimed at reaching independence from Russian fossil fuels, and a joint Task Force on Energy Security was established to set out cooperation parameters. Current U.S.-EU strategic energy cooperation is still hampered by factors such as natural gas trade inertia, US liquefied natural gas (LNG) capacity, and differences within EU member states. However, the political will demonstrated by the U.S. and the European Commission has destabilized EU-Russia energy cooperation and created far-reaching implications for the EU’s energy, industrial and monetary strategies.

1. The EU May Become Dependent on US Energy.

After the end of the Cold War, the EU took the initiative to start energy cooperation with Russia. Behind the move lay a rational energy and security policy: the EU was already Russia’s largest energy importer and therefore Russia did not threaten EU security. As a result, the possible security threats posed from the East were further alleviated and the EU could earmark huge financial expenditures, otherwise used for national defense, to further economic development.

Unlike importing from the Middle East, Russian energy imports offered both lower costs and improved supply stability, which boosted the international competitiveness of Europe’s economy. In other words, EU-Russia energy cooperation helped lay the foundation for EU strategic autonomy. Despite pressure from the U.S., the former German Chancellor Angela Merkel pushed forward the Nord Stream 2 natural gas pipeline project to increase the stable natural gas supply directly from Russia and to bypass Poland and Ukraine, which were both susceptible to US influence.

Not only has the U.S. frowned upon the EU’s implementation of strategic autonomy but it has actively sought opportunities to interrupt EU-Russia energy cooperation. In recent years, the U.S. had peddled its shale oil and gas to the EU on the pretext of “enhancing European energy security,” while obscuring its real agenda of forcing Russian energy out of the EU market.

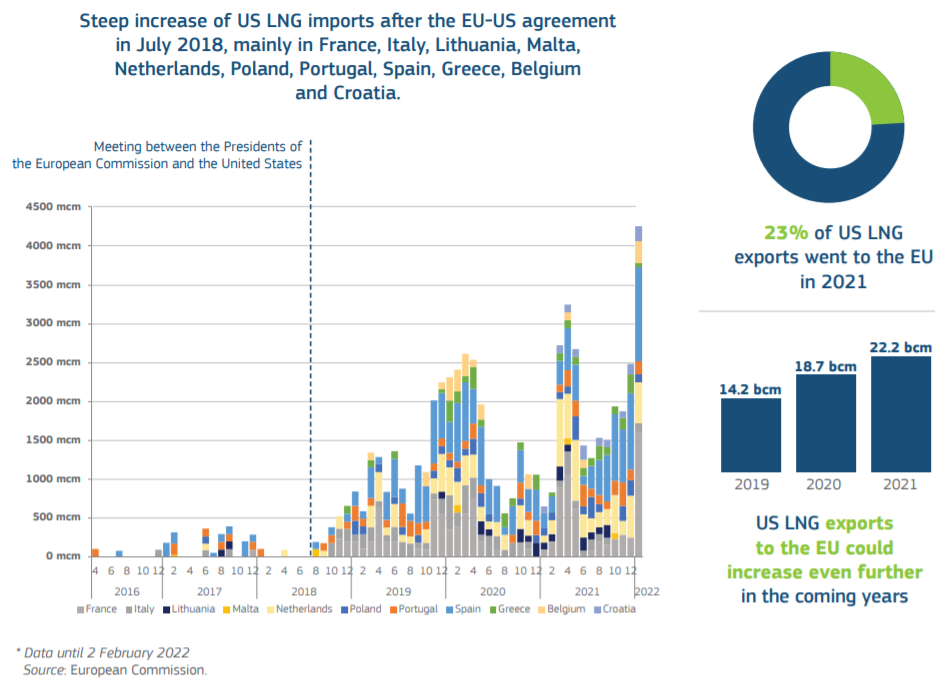

Currently, Russian energy takes up more market share than US energy within the EU market. In 2021, the EU had imported 155 bcm of natural gas from Russia - consisting of 140 bcm of pipeline natural gas and 15 bcm of LNG - accounting for 45% of its total natural gas imports. Even though the total volume of US LNG exports to the EU hit a new high during the same period, totalling 22 bcm, it accounted for only 6% of the EU’s total natural gas imports.

However, on March 25th, 2022, the President of the European Commission, Ursula von der Leyen, and US President Joe Biden issued a joint statement on European energy security, which demonstrated the political will of the European Commission to shift its energy dependence from Russia to the U.S.

The new U.S.-EU energy arrangement will see the United States strive to ensure additional liquified natural gas (LNG) volumes for the EU market of at least 15 bcm in 2022 with further expected increases over time. As such, the U.S. has practically declared that it intends to replace all Russian LNG orders with the EU, which in 2021, had also amounted to 15 bcm of LNG. In fact, a senior US government official made a public statement that the U.S.-EU energy pact was “aiming to make the EU independent from Russian LNG in a very short period of time.”

In addition to the above arrangements, the European Commission has indicated it will work with EU member states toward ensuring stable demand for additional US LNG of approximately 50 bcm per annum until at least 2030. In the REPowerEU plan submitted on March 8th, the European Commission proposed that the EU import an additional 50 bcm of LNG from Qatar, the U.S., Egypt, West Africa, and other places each year. According to the joint statement, the European Commission appears to have allocated all the “quota” for additional LNG imports to the U.S. Were the above plan to be implemented and the EU to successfully reduce natural gas demand by 100 bcm by 2030, US LNG would account for about 30% of the EU’s total natural gas imports at that time.

The two sides also confirmed their joint resolve to terminate EU dependence on Russian fossil fuels by 2027. This has interrupted the EU’s longstanding strategy of achieving “energy independence” through EU-Russia energy cooperation over the past three decades and substantially increased EU susceptibility of being “manipulated” by the U.S. in both energy and finance.

2. The Competitiveness of European Industries May Decline.

In recent years, and especially since the outbreak of the COVID-19 pandemic, both the U.S. and the EU have come to realize the importance of re-industrialization. While they remain staunch alliance partners, the U.S. and EU are now engaged in the zero-sum game of vying to attract industrial companies back to their respective domestic markets. The U.S. has transformed itself into an energy exporter, and it overshadows the EU in terms of financial strength. However, the extent to which the US industrial chain has been hollowed out is far more serious than that of the EU. Therefore, access to affordable and stable energy supply has become a key area for both sides as they compete over the process of re-industrialization.

(Source: European Commission)

(Source: EIA, Energy Intelligence Group)

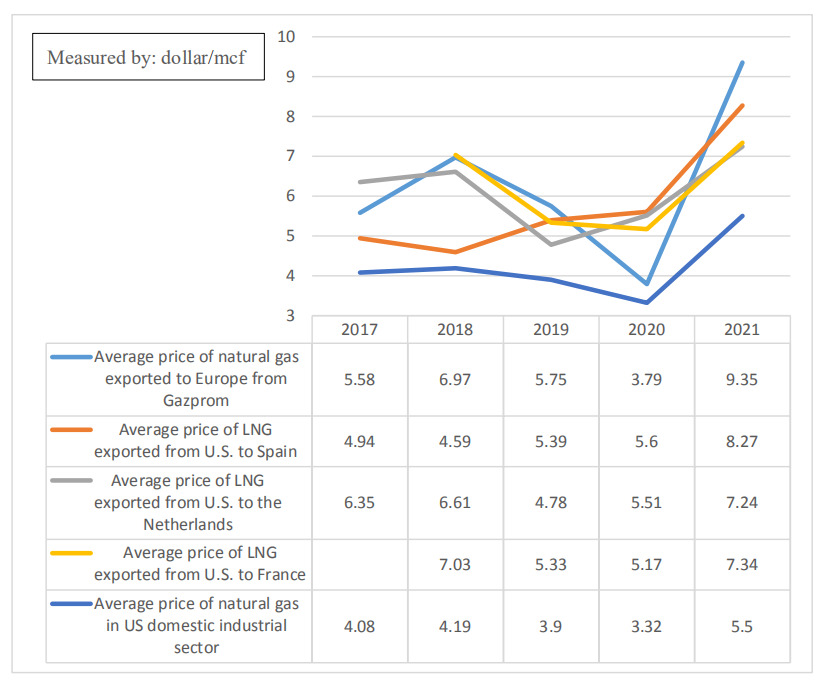

As an energy importer, the EU is in a relatively disadvantageous position. The chart above shows that after the U.S.-EU declaration of July 2018, when US LNG first entered the EU market, the average price of natural gas exported from Gazprom to Europe was relatively high. In 2019, Spain, France, and the Netherlands, positioned along the Atlantic coast, became the top three buyers of US LNG within the EU, a position they retain today. (NB: the Netherlands bought more than France in 2021.)

In mid-2021, the EU began promoting the Fit-for-55 package and the Carbon Border Adjustment Mechanism (CBAM), in an attempt to apply the cost-effective Russian pipeline natural gas imported since 2020 as an industrial “pain reliever” during its green economy transition. After its transition, the EU levied massive carbon tariffs on energy-exporting countries, which forced the average price of Gazprom’s LNG higher than that of US LNG exported to Spain, the Netherlands, and France. As such, the fact that the European Commission shifted to US LNG holds certain economic justification but does not counterbalance the significant risk of increased dependency on US energy.

More importantly, once the U.S. and Europe develop a stable LNG supply and demand relationship, the EU economy will most likely face the predicament of higher manufacturing costs and lower industrial competitiveness compared with the U.S. After all, the average price of natural gas in the domestic industrial sector of the U.S. is much lower than that of the LNG exported from the U.S. to Spain, the Netherlands, and France. Unlike Russia’s pipeline natural gas, which has already received the initial infrastructure investment, the EU’s imports of LNG entail shipping costs and the costs of building and operating LNG terminals. After the outbreak of the Russia-Ukraine conflict, the construction cost of the Brunsbuttel LNG terminal in Germany rose to over one billion euros, far exceeding the previously estimated 450 million euros.

In addition, the energy price induced a decline in EU industrial competitiveness and the security risks posed by the Russia-Ukraine conflict increased the likelihood that industry would gravitate from developing countries to the U.S., instead of the EU. Not only will this put the EU in a disadvantageous position in the re-industrialization competition with the U.S., but it will have far-reaching impacts on the EU economy. The combination of a weakened re-industrialization of the EU, higher than expected interest rate hikes by the US Federal Reserve, and capital flight from the EU, caused by the Russia-Ukraine conflict, may further weaken the stimulating effect of investment on the EU economy. As such, the impact of high inflation in the eurozone, which reached 7.5% in March 2022, indicates the potential of EU member states to repeat the mistakes of other developed countries at the end of the last century and fall into stagflation where government intervention fails to reverse economic contraction.

3. Dollar Dominance Against the Euro May Consolidate Further.

Since its introduction, the euro has challenged dollar dominance. The settlement method of commodity transactions, whether in dollars or in euros, directly affects the proportion and status of the currency in the international payment system. Since the trade between the EU and Russia can be settled in euros, EU-Russia energy cooperation not only increased the use of the euro in the international community but also reduced the dollar reserves of EU member states for energy purchases. Recently, German Chancellor Olaf Scholz reiterated that Germany refuses to buy natural gas from Russia in rubles, pointing out that most German natural gas supply contracts specify payment in euros, with only a small proportion denominated in dollars.

In the wake of the Russia-Ukraine conflict, Germany not only suspended the certification process of the German-Russian Nord Stream 2 project but also decided to build a new LNG terminal in Brunsbuttel with a capacity of 8 bcm per annum, designed to support the huge new demand for LNG imports from countries other than Russia. If the March 25th joint statement of the United States and the European Commission is implemented, both sides may have additional LNG orders of up to 15 bcm in 2022, possibly reaching 50 bcm per annum until at least 2030. These LNG orders will most likely be settled in dollars rather than euros, which will have a severe impact on the euro’s international status.

© 2013-2021 Taihe Institute (TI) . All rights reserved. Taihe Institute (TI) .京ICP备16023694号-1

Privacy Policy丨Terms of Service

Contact Us: public@taiheglobal.org